WEEKLY E-MAIL

REPORTING SEASON WRAP-UP – AUGUST 2025

By Karen Maher

August reporting season for Australian markets recently concluded. This period provides valuable insights into how businesses are navigating current economic conditions and what they expect moving forward.

55% of companies delivered results in line with market expectations – well above the five-year average of 39%. Just under a quarter missed expectations, while 21% beat them.

Over August, the benchmark ASX 200 index gained 2.6%, repeatedly hitting fresh highs.

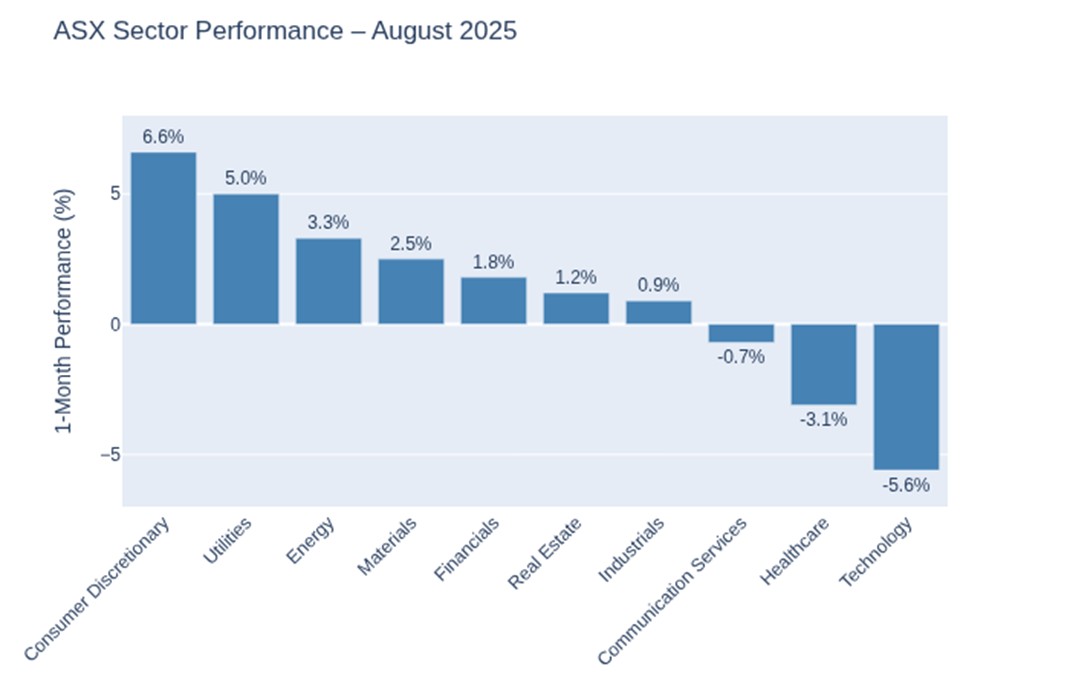

The best-performing sector was consumer discretionary, supported by strong results from retailers and travel-related companies. The healthcare and technology sectors were among the weakest, with several large-cap names missing expectations.

The chart below shows the 1-month performance of each ASX sector to 31 August 2025:

CBA continued to outperform with solid earnings and dividend growth, though analysts note a disconnect between its valuation and underlying fundamentals, suggesting a potential pullback.

Large-cap stocks like CSL saw sharp declines due to weaker earnings and cautious outlooks.

The materials sector faced headwinds from falling commodity prices and global trade uncertainty. Despite this, companies like BHP and Rio Tinto increased capital expenditure in copper and lithium projects, positioning for long-term growth. The sector remains sensitive to geopolitical developments and China’s economic outlook.

Dividend payouts were slightly lower than last year, with ASX 200 companies expected to distribute around $38 billion in dividends, slightly down from the previous year. Several companies, including Telstra and Wesfarmers, announced special dividends or buybacks, reflecting strong balance sheets and shareholder focus.

Heightened volatility during reporting season was driven by:

- Trade tensions between the US and China

- Interest rate cuts by the RBA, which boosted property-related stocks

- Stretched valuations across many sectors, prompting cautious investor sentiment

The outlook for the remainder of 2025 remains cautious. Inflationary pressures, cost constraints, and conservative earnings guidance suggest slower growth ahead. However, opportunities remain for long-term investors, particularly in sectors with strong fundamentals and strategic reinvestment plans.

Karen Maher

Associate

SMSF Specialist Advisor™

If you have any questions or comments, please email me at karen@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

3 Mar 2026

23 Feb 2026

2 Feb 2026