WEEKLY E-MAIL

EVERGRANDE DEBT CRISIS

By Ngoc Christodoulou

Source: Bloomberg

Evergrande Group is China’s second-largest property developer. It has a diverse business that includes wealth management, food manufacturing, electric vehicle production, sports & theme parks, and property development. It is listed on the Hong Kong Hang Seng Stock Exchange and employs over 200,000 workers. Evergrande has enjoyed a decade of growth but is China’s most indebted company and is on the verge of collapse as it is struggling to service debts exceeding US$300 billion.

Evergrande’s debt crisis has triggered concerns about the ongoing strength of China’s property market, including construction activity and the knock-on effect on global growth and share markets.

Effect on Iron Ore

China is Australia’s largest trading partner.

China has previously reduced its steel manufacturing, a high energy process, to meet 2060 net-zero carbon emissions targets. Evergrande’s collapse could also dampen property development in China and further reduce the demand for construction materials such as steel, made mostly from imported iron ore. China is the world’s biggest producer of steel and accounts for nearly 70% of the global iron ore imports, of which 60% are imported from Australia.

Australian iron ore exports were an estimated $149 billion in the 2020-2021 Financial Year, of which 75% went to China.

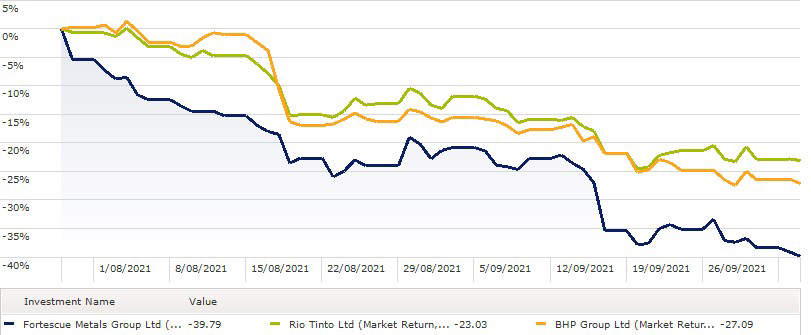

Iron ore prices have halved since July 2021 from $US200/tonne to $US117/tonne, causing a fall in the share prices of Australia’s largest mining companies – BHP, Rio Tinto and Fortescue Metals.

Effect on Exports

China is Australia’s biggest export market, even with the removal of iron ore exports. The collapse of Evergrande could affect China’s economy, impacting consumer confidence and spending, which could decrease domestic demand for other goods and services.

Even though Evergrande’s debt is localised in China, it adds to the volatility of global financial markets, with the Australian share market falling off its highs over the last couple of weeks. Hong Kong’s Hang Seng Index fell 0.4%, and Japan’s Nikkei 225 Index fell 1.2% on Monday 4 October 2021, with Evergrande shares in a trading halt.

What will happen?

Evergrande’s sheer size, as well as the amount of debt it owes, has caused fears of contagion. The massive loan obligations have evoked comparisons with the Global Financial Crisis (GFC), where issues in the property sector almost crashed the US financial system.

While Evergrande defaulting on their debt is a near-certainty, we believe that the risks of a GFC-style spillover are overblown.

Preventing financial contagion will be the priority for the Chinese government. Evergrande owes a significant portion of its liabilities to small businesses, homebuyers, and even employees. Their wealth will face severe implications in the case of a disorderly resolution. Therefore, we think this is an unlikely route for Chinese authorities to take.

The People’s Bank of China has conducted regular stress tests on bank liquidity since 2009. It has recently tested for specific property exposures earlier this year. The “Three Red Lines” policy has probably had a major role in exacerbating Evergrande’s liquidity issues. Therefore, we believe that the government is aware of any risks present and are prepared for them.

We think that the Chinese authorities are backing themselves to resolve the issue. The Chinese government has dealt with high-profile defaults. A similar approach is expected with Evergrande.

The likely resolution method is a combination of government intervention, debt restructuring, and various entities being requested to step in and conduct “national service”. The government’s behaviour so far has backed this up. They have pledged to ensure social stability and have moved accordingly, injecting liquidity into the banking system and supporting smaller regional banks that have excessive exposure to Evergrande.

Ngoc Christodoulou

Associate Financial Planner

Authorised Representative No. 1271825

If you have any questions or comments, please email me at ngoc@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026