WEEKLY E-MAIL

RBA HOLDS RATES STEADY

By Ethan Hardeman

In its September 2025 meeting, the Reserve Bank of Australia (RBA) opted to keep its cash rate unchanged at 3.60%, pausing further monetary easing for the time being. The decision comes after three separate 25-basis-point rate cuts earlier in the year (in February, May, and August), down from a peak of 4.35% before the February board meeting.

The decision to hold rates was widely anticipated by markets and economists alike, with all 39 economists polled by Reuters expecting no change. Still, commentary from RBA Governor, Michelle Bullock, suggests caution, and potentially a less aggressive path in future rate cuts than economists and homeowners had previously hoped.

Why did the RBA hold interest rates?

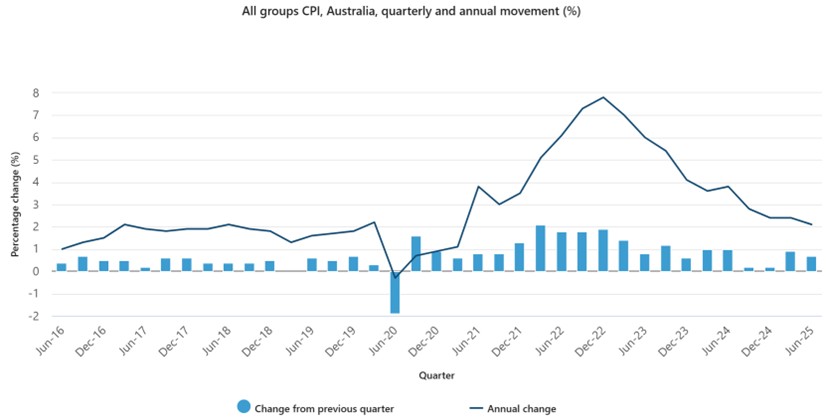

The RBA’s decision to hold interest rates stems from a mix of inflationary dynamics, lagged effects of earlier rate cuts and stable conditions in the labour market. Whilst headline inflation has eased from its 2022 peaks, recent figures show renewed persistence, with the August Consumer Price Index (CPI) result rising 3% year-on-year – its highest level since July 2022.

Source: Australian Bureau of Statistics

The RBA remain particularly vigilant on inflation in sectors such as housing and services, which are typically slower to adjust. The trimmed-mean inflation measure, which removes volatile items to understand underlying inflation better, remains above the midpoint of its target band.

Simultaneously, the RBA aims to allow more time for its earlier rate reductions to be reflected in consumer spending, investment, and housing demand. The unemployment rate remains near 4.2% and wage growth, though moderate, continues to pose some risk if demand strengthens. Taken together, these dynamics prompted the RBA to stress a cautious “meeting by meeting” approach rather than committing to future cuts.

How did the market and public react?

The ASX 200 saw a modest dip, reflecting caution amongst investors in rate-sensitive sectors. Financials, in particular, were weighed as banks grapple with margins in a lower-rate environment.

However, mortgage holders will have to wait until mid-November for any chance at another rate cut. Interest rate swaps now imply a reduced probability of a rate cut at the next meeting, down to 36%, compared to 55% previously.

What comes next?

The RBA has made it explicitly clear that future cuts will depend heavily on incoming inflation and labour market data, particularly the September and December CPI releases.

Whilst another rate cut this calendar year is not impossible, forecasts are being scaled back, and many analysts expect the next sustained round of cuts will begin in 2026, unless inflation falls quicker than anticipated.

Ethan Hardeman

Junior Paraplanner

If you have any questions or comments, please email me at ethan@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

3 Mar 2026

23 Feb 2026

2 Feb 2026