WEEKLY E-MAIL

WHY THIS PROPERTY DOWNTURN WILL BE DIFFERENT

By Paul Nicol

Residential property has benefited from the long-term downtrend in interest rates since the 1980s and now appears far more vulnerable to the reversal than in previous downturns. In the last 25 years, residential property price downturns have mostly been mild, with prices falling less than 10%, and these downturns have been brief, with prices quickly rebounding. This cycle appears different thanks to a combination of high household debt levels, high home price to income levels, an end to the long-term downtrend in interest rates and the elevated prices achieved during the pandemic.

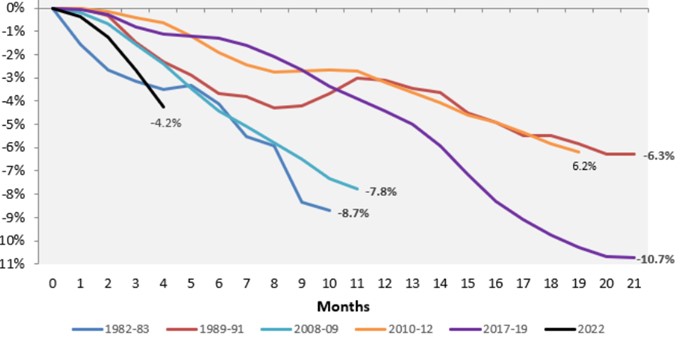

According to CoreLogic, Australian residential dwelling prices fell another 1.6% on average in August. This was the fourth monthly decline in a row and the fastest monthly decline since the early 1980s recession. After surging 28.6% between the pandemic low in September 2020 to the high in April, average residential property prices have now fallen 3.5%, comparable to the pace of decline over four months going into the 1980s & 1990s recessions and the GFC. The result is worse for capital cities, with the 5-City Peak to Trough now down by 4.2% in the last four months.

5-City Peak-to-Trough Declines

Source: CoreLogic

Forecasters now agree that residential dwelling prices will fall more significantly than in previous cycles.

As rising mortgage rates impact, AMP Capital expects national average property prices to fall 15-20% from top to bottom in the next 12 months. AMP believes a surge in fixed rate loan expiries risks a sharp rise in distressed selling as up to a quarter of borrowers will roll over into much higher mortgage rates in the upcoming period.

ANZ’s economists expect the RBA to continue its aggressive increase in the cash rate with a cash rate target to 3.35 per cent before the end of the year. This would send typical variable mortgage interest rates close to 6 per cent. They expect capital city prices to fall 18 per cent over the balance of 2022 and 2023.

These forecasts are in line with other major financial institutions, with Commonwealth Bank’s economists expecting a decline of at least 15 per cent, even if the RBA cash rate only reaches CBA’s forecast of 2.6 per cent, which is lower than market expectations.

ANZ’s said a tight rental market, rising immigration and low unemployment would help to mitigate the decline. However, it would take a reduction in interest rates to see the market start to turn around.

In New Zealand, Auckland properties surged in value until the middle of last year. Then, the Reserve Bank of New Zealand (RBNZ) flagged it was likely to start lifting the official cash rate to try & control inflation.

Last week, the RBNZ again lifted the official cash rate, taking it to 3%.

New Zealanders have been impacted by higher interest rates seven months before the RBA started down a similar path.

House prices in Auckland are down 15 per cent from their peak last year, according to Infometrics data. By the same measure, the national average is down 9.6 per cent. The RBNZ is now predicting a peak to trough of nearly 20 per cent.

In Australia, the downtrend in interest rates between 1990 and 2021 enabled home buyers to borrow more & pay more for homes. A poor dwelling supply response in the face of strong population growth since the mid-2000s enabled rapid price gains to persist.

The long-term bull market in property prices from the 1990s was underpinned by a shift from low to high home prices to incomes, a similar change in household debt relative to incomes and a long-term downtrend in interest rates. These are likely to have run their course.

The latest dwelling value data is difficult for anybody who recently borrowed heavily to purchase a residential property. We believe caution is warranted for anybody considering a residential property investment until the RBA’s aggressiveness on interest rates ends. Until then, we can expect to see the trend of residential property price falls to continue.

Paul Nicol

Managing Partner

Senior Financial Planner

SMSF Specialist Advisor™

Barron’s Top Financial Adviser 2017-2021

Authorised Representative No. 230876

If you have any questions or comments, please email me at paul@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026