WEEKLY E-MAIL

WHEN WILL INTEREST RATES START TO RISE?

By Sam Eley

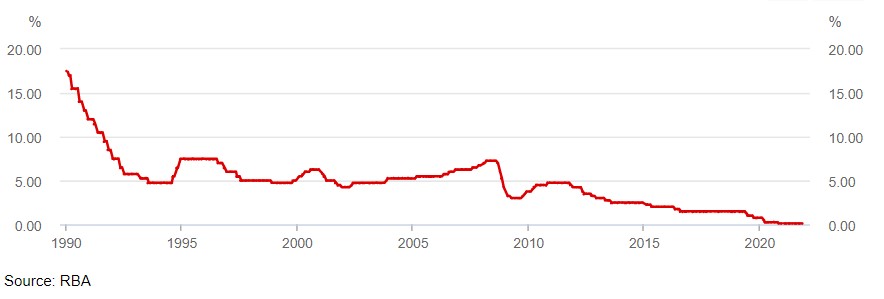

It seems hard to fathom now, but the RBA Cash Rate was 7.00% in September 2008. While the interest rate cuts at that time were amid the Global Financial Crisis, since then, we have seen a steady decline in interest rates to where we sit today at a record low of 0.10%. It has been held at 0.10% by the RBA since November 2020. Official cash interest rates have been below 1.00% since October 2019, now two full calendar years. I’m sure many investors long for the return of 7.00% p.a. term deposits, which now seem too good to be true!

RBA Cash Rate Target

While this reduction in interest rates is good news for borrowers and those with large mortgages, it is extra tough for first home buyers looking to enter the housing market and retirees who are dependent on their capital to fund their lifestyle in retirement.

With the average house price growth in Melbourne up 13.10% in 2021 despite continued COVID-19 lockdowns, the ability for first home buyers to get into the housing market is becoming increasingly unattainable. The RBA is under pressure to raise interest rates to curb the sharp rise in house price growth, but to this point are reluctant to move given wage growth is not within target ranges. The RBA is putting the onus on responsible lending standards and an increase to interest rate serviceability targets to reduce borrowing capacity.

Retirees who are dependent on the defensive part of their portfolio to earn significant interest income are also in a tough predicament. They have to accept a lower return than previously hoped for on their defensive assets or take increased risks to garner a better return. This can put the longevity of capital into question, increase volatility and run the risk of being invested in a portfolio that is not suitable to their risk tolerance levels.

In their 3rd November 2021 meeting, the RBA mentioned they expect the Australian economy to bounce back relatively quickly due to eased COVID-19 restrictions and increased vaccination rates. There is an expectation that Gross Domestic Product (GDP) growth will be at 3.00% for 2021, and unemployment will begin to decrease to 4.25% by the end of 2022.

Inflation has begun to pick up on the back of higher fuel prices, higher prices for newly constructed homes and global supply chain disruptions, with the headline figure now at 2.10%. The RBA notes that while they are mindful that inflation has picked up, it’s still low in underlying terms and less than many other countries due to Australia’s low wage growth. Wage growth may begin to pick up on the back of firms competing more aggressively for skills shortages, as well as an increase in migration on the back of borders opening up.

The RBA has been undertaking a yield curve control strategy since March 2020 to keep the three-year bond yield at 0.1%. Under yield curve control, a central bank promises to buy as many bonds as needed to keep yields below a certain level. That allows it to control longer-term interest rates. The RBA has now let the three-year yield target rise through their cap, which is part of the reason we see speculation in the market of rate rises before 2024.

This is also on the back of comments made by Philip Lowe (Governor of the RBA), indicating that the Australian economy has made earlier-than-expected progress towards the inflation target of 2.50%. On the back of the abandonment of the yield curve control and comments on inflation, we are already beginning to see lenders raise their fixed interest rates for 2-5-year periods on the back of these announcements.

The RBA wants to see inflation get sustainably back to 2.50% per cent, with wage growth at 3.00%, before increasing interest rates. While this is currently forecast for the end of 2023 or the beginning of 2024, many view the RBA abandoning their yield curve control strategy to indicate that an interest rate rise is coming earlier than forecast.

Sam Eley

Senior Financial Planner

Authorised Representative No. 1234685

If you have any questions or comments, please email me at sam@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026