WEEKLY E-MAIL

A DYNAMIC APPROACH TO RETIREMENT INCOME

By Jonathan Toh

For most retirees, particularly those early in their retirement, determining how much can safely be drawn from their portfolio can be challenging and requires careful consideration. Finding the right balance between meeting one’s spending needs while also making sure sufficient capital remains for their later retirement years can be a difficult balance to maintain.

A study by Vanguard in 2018 looked into retiree spending in detail, and separated a retiree’s goals into four primary categories:

- Basic Living Expenses – The base amount of income needed to cover your core non-discretionary expenses, such as groceries, rates and bills etc.

- Contingency Reserve – A cash buffer, generally held in banks to address unexpected expenses.

- Discretionary Spending – The ‘wants’ in spending, allow to maintain the preferred lifestyle in retirement.

- Legacy – The transfer of wealth to beneficiaries Each retiree will place a different emphasis to each of these primary categories, but ultimately it can provide a guide on how retirement spending can be approached.

There are a number of “rules” that can assist in determining a safe drawdown level on capital to fund retirement lifestyle.

“Dollar plus inflation” rule

A popular strategy known as the “dollar plus inflation” or “4% spending” rule developed by William Bengen (1994), suggests a retiree will set an initial dollar amount to spend from the portfolio and increase the drawdown amount by the amount of inflation each year.

Although this approach is simple to implement and provides stable income year to year, it is not without its shortcomings. Given its static approach, it runs the risk of either premature portfolio depletion or lifetime under-consumption due to what is known as “sequence of returns risk”, in which the drawdown continues to operate regardless of the portfolio returns.

This static drawdown approach could result in a retiree either missing out on enjoying retirement by underspending or overspending and depleting the portfolio too soon.

“Percentage of portfolio” rule

Another popular spending rule is the “percentage of portfolio” rule, this rule suggests that a retiree will spend a fixed percentage of the portfolio balance, adjusting for the increase or decrease based on the portfolio performance.

The benefit of this drawdown rule ensures a retiree’s portfolio will not be depleted, however, it does mean the annual spending amount can fluctuate significantly, which may not be appropriate for retirees with basic living expenses that are relatively high proportion of their total expenses.

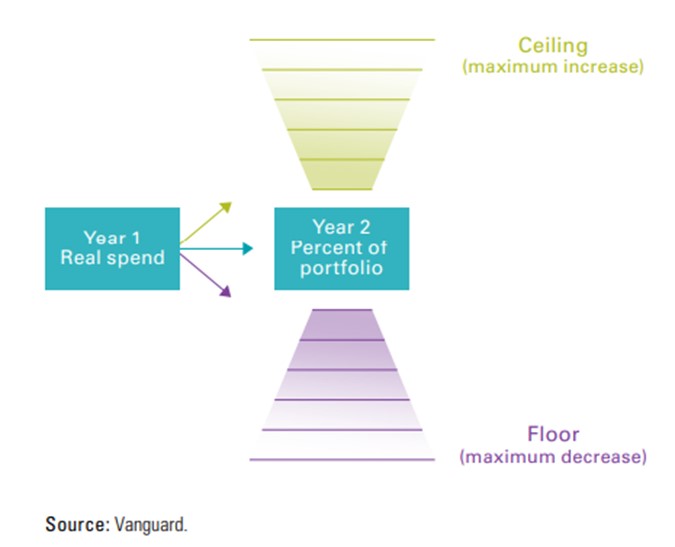

“Dynamic spending” rule

A hybrid approach combining the previous two rules, known as the “Dynamic spending” rule, provides the customisation necessary for each retiree’s situation. It allows for spending to fluctuate based on the portfolio performance, whilst moderating fluctuations in spending year on year. This is done by placing a “ceiling”, the maximum drawdown rate from the portfolio allowable and a “floor” the minimum rate from the portfolio allowable.

This rule allows retiree to benefit from an outperformance by spending a portion of the gains, while weathering the underperformance without a significant reduction in spending.

Ultimately, each individual’s situation is unique. Developing an appropriate spending strategy is key to reducing the likelihood of outliving your savings, whilst simultaneously enjoying retirement to the fullest extent.

Jonathan Toh

Associate Financial Planner

Authorised Representative No. 1284667

If you have any questions or comments, please email me at jonathan@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026