WEEKLY E-MAIL

WHAT HAS HAPPENED TO THE CHINESE ECONOMY?

By Paul Nicol

The Chinese economy was expected to rebound strongly in late 2022 and through 2023 as it reopened from its multi-year COVID lockdowns, coupled with material government stimulus to support the flailing property sector instigated at the same time as the reopening.

However, the bounce has been underwhelming versus expectations that China’s recovery would be a saviour for slowing developed economies.

Unlike other countries that have seen consumer spending shift from goods to services as the economy reopens, this was more muted for China, with manufacturing output also disappointing amid ongoing cautious sentiment around the recovery of the property sector.

Recent data from China supports the view of a Chinese economy struggling to stave off deflation and on the cusp of a Japanese-style lost economic decade. China’s current core inflation, which excludes food and fast-dropping energy prices, has been lower only in the pandemic and the 2008-09 Global Financial Crisis, according to data starting in 2008. Economic growth in this year’s second quarter was just 3.2% annualized, lower than any period from the financial crisis to the pandemic. Inflation last month hit zero, and the monthly figures are down for five months in a row, the most prolonged period since 2003. Manufacturing output, exports, and investment are all falling. Youth unemployment has risen to 20.8% in May.

The Chinese government appears to be in an economic-policy box, having spent the last decade pursuing a highly unbalanced growth model. The result was an enormous property and credit-market bubble that is now at the heart of China’s economic malaise. Further monetary and fiscal policy support to the housing market might provide short-term economic relief. However, that would exacerbate the eventual day of reckoning from the property and credit market bubbles that formed in China. The central bank might consider aggressive interest-rate cuts. But causing the Chinese currency to depreciate might invite further U.S. trade restrictions. The Chinese currency has depreciated by around 7% against the dollar over the past year.

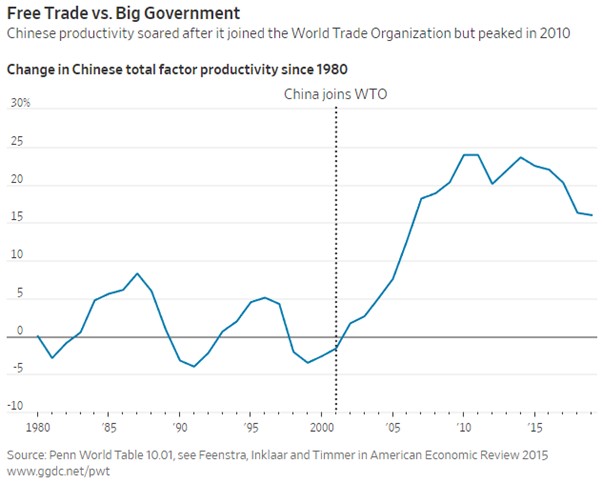

A bigger picture problem for China is its workforce is shrinking and aging. China’s population began to shrink last year, and productivity has been falling for more than a decade after an extraordinary growth period following China’s entry into the World Trade Organization in 2001.

Weak earnings and low share prices in China appear to be the natural byproduct of weak productivity, and it seems to continue to throw debt at the problem is not a solution.

The question is, will China become a much bigger and uglier version of Japan?

Paul Nicol

Managing Partner

Senior Financial Planner

SMSF Specialist Advisor™

Barron’s Top Financial Adviser 2017-2021

Authorised Representative No. 230876

If you have any questions or comments, please email me at paul@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026