WEEKLY E-MAIL

RESIDENTIAL PROPERTY – WHAT DO RATE RISES MEAN FOR RESIDENTIAL PROPERTY PRICES?

By Sam Eley

Over the past few years, we have seen a meteoric rise in residential property prices. We’ve all witnessed it – whether it’s showing up to ‘sticky beak’ at auctions, pleasant surprises when selling homes, or the struggle in trying to help your children into their first homes. This has been spurred by a number of factors – chief of all, the record low interest rates that have been on offer the past few years. The cheaper debt is, the more someone can afford to spend to purchase a property – or stretch themselves to get into their ‘dream home’.

Now, the perfect storm essentially occurred. Low supply has meant more buyers turning up to auctions with deeper pockets, buyers are sitting on larger cash deposits after COVID lockdowns impacting their spending ability, people who already own a home, after spending more time there during lockdowns have decided to upgrade , or move to coastal or regional areas, or downsize. The last two years with significant time spent working from home has also spurred many of these lifestyle-based decisions.

The RBA had initially forecast rates to rise by 2024, wanting to wait until wage growth hit their 2-3% target before progressively increasing interest rates to keep pace with inflation. In the US, inflation numbers released in February 2022 indicated that CPI had risen 7.9% over the proceeding 12 months – leading to the US increasing rates by 0.25%, the first rate rise since December 2018. Most major banks are now forecasting Australia to follow suit, with rate rises expected from June 2022.

The RBA has to walk a fine line. While interest rate rises will be needed to cool down the economy and slow the price growth of costs of goods, the reality is that Australian household debt as a proportion of disposable income is at its highest level in history. If the RBA raises interest rates too high, it will slow economic growth and put pressure on the housing market, which, for many people, their largest amount of equity is. The RBA’s gradual raising of interest rates will undoubtedly put pressure on households, and conservative raises over the next year or two will be the intention of the RBA, to see how the economy responds.

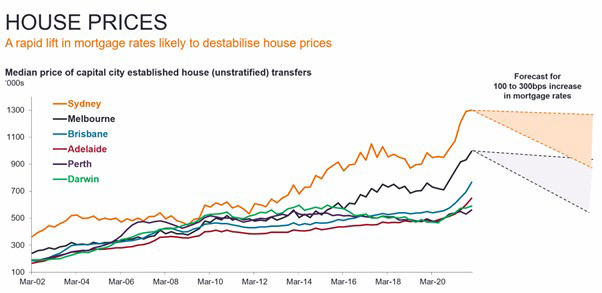

What this will mean for house prices likely depends on the severity of future rate increases:

Source: Janus Genderson Investors, ABS, to December 2021

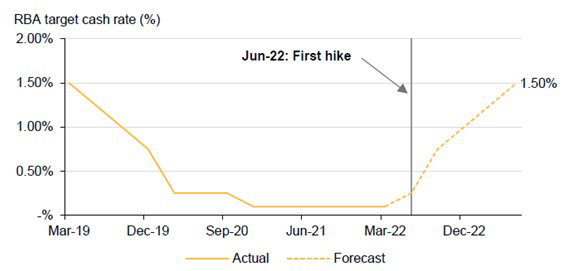

Macquarie’s Macro Strategy team are tipping that rates should progressively move to around 1.5% in calendar year 2023. This would lift rates back to where they were in March 2019, and while not exactly a windfall for savers, it would certainly look more attractive than the current 0.1% on offer, albeit will still be significantly below the expected inflation numbers.

Source: Macquarie Macro Strategy, April 2022

Based on a 1.5% cash rate target, Macquarie are forecasting a 10% decline in national housing prices as the RBA begins to increase rates.

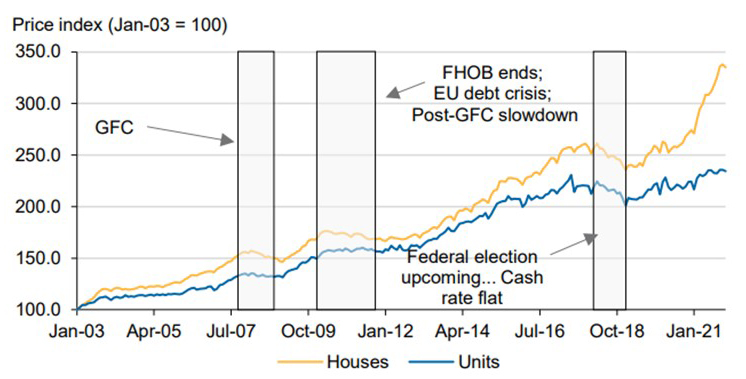

While it may not feel like it, residential property markets have experienced other downturns over the past 20 years too:

Source: APM, Macquarie Research, April 2022

In 2007-2008, the Global Financial Crisis (GFC) decline was led by a worldwide moderation of credit availability and a broader global recession. The Post-GFC decline in 2010-2012 was led by a reduction, and then ceasing, of the First Home Owners Boost (FHOB), as well as the European Debt Crisis and cash rate rises. The 2018-2019 decline occurred in the lead up to the 2019 Federal Election, which Labour was tipped to win, that would have led to a reduction in the capital gains tax discount to 25% from 50%. The Coalition ultimately won the election, and the discount reduction was scrapped.

Ultimately, the scope of house price weakness from 2022 onwards will depend on how tight monetary policy gets, and the economy’s ability to absorb the flow-on effects of higher inflationary inputs.

Sam Eley

Senior Financial Planner

Authorised Representative No. 1234685

If you have any questions or comments, please email me at sam@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026