WEEKLY E-MAIL

DECEMBER INFLATION RISE AND WHAT TO EXPECT FROM THE RBA

By Amelia Paullo

Over the past week, several important pieces of economic data have been released that provide insight into Australia’s inflation outlook and what we may expect from the Reserve Bank of Australia (RBA) at its upcoming meeting on 3 February.

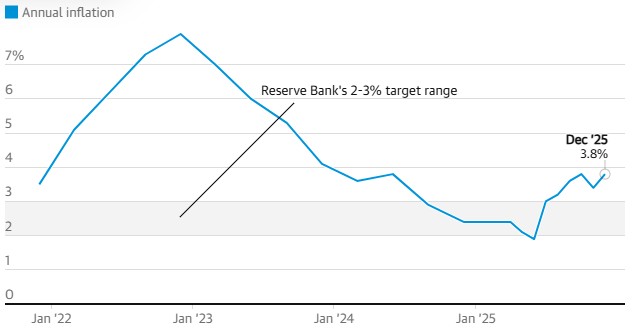

Australia’s annual inflation rate rose to 3.8% in December, up from 3.4% in November, with the result higher than economists had expected. This reflects a broader lift in price pressures across the economy and continues to show that inflation is proving more persistent than the RBA would like.

Source: ABS

A significant driver of this increase was the continued rise in housing related costs, particularly energy prices. Electricity prices surged 21.5% over the year as state energy subsidies rolled off in Queensland and Western Australia. This contributed to inflation running hottest in Brisbane (5.2%) and Perth (4.4%), the highest among major cities. Rental costs rose 3.9% over the year, slightly lower than the previous month’s reading, supported by relatively stable vacancy rates. Supermarket pressures also remained, with food and non alcoholic beverages up 3.4% over the year.

The ABS also highlighted a nearly 10% jump in travel and accommodation prices, driven by strong December demand during the summer holiday period.

When looking at underlying inflation, the RBA’s preferred measure, the trimmed mean, rose 3.4% over the year, up from 3% in the September quarter. This indicates that even once volatile components are removed, inflation remains elevated and above the RBA’s target range of 2-3% p/a.

In addition to the inflation data, last week’s strong employment figures showed the unemployment rate falling to 4.1%, its lowest level in seven months. Together, these stronger than expected numbers have shifted market expectations around interest rates. NAB now estimates around a 75% probability of a rate rise next week, up from around 60% prior to the inflation data release.

Reflecting these shifting expectations, the Australian dollar briefly climbed back above US 70 cents, supported by both the robust labour market data and increased likelihood of near term policy tightening. While it has eased somewhat since, the currency remains stronger than in earlier months.

We will continue to monitor these changes closely, and continue to review our portfolio assets and the potential impact of rising rates.

Amelia Paullo

Senior Financial Planner

SMSF Specialist Advisor™

Authorised Representative No. 1243426

If you have any questions or comments, please email me at amelia@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026