WEEKLY E-MAIL

MARCH US INFLATION REPORT – A DELAYED START OF THE INTEREST RATE EASING CYCLE?

By James Malliaros

Since June 2023, investor sentiment has been boosted by the idea of interest rate cuts on the horizon in the US as the pace of inflation was showing signs of slowing. Last week however, US CPI figures for March came in hotter than expected, resulting in the nation’s inflation rate rising for a second straight month to an annual rate of 3.5%. Not only was this above the 3.2% economists were expecting, but the market also got the jitters as investor hopes of rate cuts in June 2024 were quickly pushed back.

The main driver of inflation that dampened the rate cut outlook was the recent strong jobs data that indicated US employers hired far more employees than expected in March, whilst increasing wages at the same time. In March, 303,000 jobs were added to US payrolls which was 100,000 more than economists had anticipated. This data indicates a strong economy, and while strong, there is minimal case for the US Federal Reserve (Fed) to consider interest rate cuts. The country’s unemployment rate fell to 3.8% in March and industry specific growth has been particularly strong for hospitality businesses, with the industry’s employment back above pre-pandemic levels.

Services inflation is another sticky point for not just the Fed in the US, but most major economies around the world. Services inflation continued to outpace overall inflation to 5.3% annually in March. Supply chain issues resulting from rising geopolitical tensions as well as wages growth are the key factors behind rising services inflation.

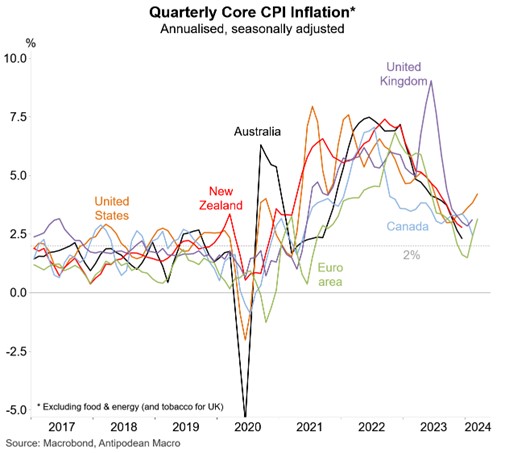

Across the developed markets, the US has now become an outlier as its inflation has bounced higher, as can be seen in the chart below. And it is the sticky services inflation that is causing central banks the most stress.

As a result, the reaction from financial markets saw stocks fall across the board, with the Dow Jones Industrial Average, the S&P500, and the Nasdaq each down around 1%. The rate sensitive sectors especially, like tech and real estate, came under huge pressure amid renewed speculation around a prolonged time before the interest rate easing cycle in the US starts.

Quite simply, stocks love lower interest rates. It increases a company’s profitability, and it supports higher valuations by investors for their stock prices. Bull markets are powered by lower interest rates, or at least the prospect of them. So, now that the market is facing the prospect of interest rates remaining higher for longer, we could experience some elevated volatility while investors adjust their expectations.

Markets are now factoring in the US rate-cutting cycle to begin in July or September rather than the previous forecast of June, pending inflation drivers ease over the next few months. Higher for longer is generally the consensus across all US Fed officials until inflation shows consistent signs of easing to the 2% target.

Although the market still believes that rate cuts will start sometime in 2024, the one thing we can be sure of is that markets are going to continue to move based upon the timing and frequency of those expected rate cuts for the foreseeable future. It’s the single most important thing on the market’s mind right now.

James Malliaros

Senior Financial Planner

Certified Financial Planner®

SMSF Specialist Advisor™

Authorised Representative No. 291633

If you have any questions or comments, please email me at james@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026