WEEKLY E-MAIL

RBA 0.25% RATE RISE

By Ngoc Christodoulou

The Reserve Bank Australia (RBA) has made its sixth consecutive cash rate rise, taking the cash rate to 2.60%. This is the fastest series of hikes since 1994.

With global inflation still running high and the prediction that inflation in Australia would exceed 7% by the end of the year, the RBA was widely predicted to supersize October’s rate hike by 0.50% last Tuesday. Whilst the rate increase was lower than expected, the RBA is still signalling more hikes, which are necessary to bring inflation back down to the forecasted 4% in 2023 and around 3% in 2024.

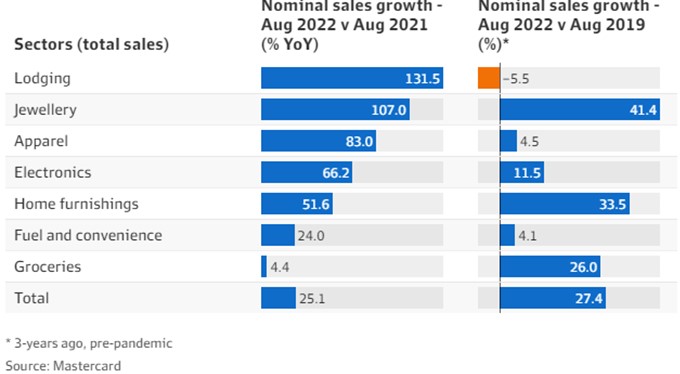

The Australian economy is continuing to grow solidly, with consumer spending still high despite recent rate rises. Mastercard reported discretionary spending increased by more than 25% in September 2022, compared to the 12 months prior and pre-pandemic levels. The RBA hopes that a sharp rise in mortgage payments for many Australians will depress spending and bring inflation to heel.

Unlike the US, where most borrowers are on 30-year fixed loans, more than 60% of Australian mortgages are variable-rate loans. The impact of recent rate increases has not yet flowed through to household cash flow due to a two to three month lag between rate changes and when banks deduct the higher monthly mortgage repayments. Australians will start to feel the impact of Tuesday’s rate change around Christmas.

While the cash rate is still considered low compared to the 1990s since 2008, many (younger) Australians have only seen low interest rates. Greater availability of credit resulting from financial deregulation plus increases in borrowing capacity due to lower repayments; have contributed to the significant surge in house prices and increased household debt levels. The vast majority of Australians now have bigger mortgages compared to their parents.

The equity market interpreted the 0.25% rise as a positive signal. It rallied by nearly 4% by the close of business on the same day as the announcement, after weakness that saw the S&P/ASX 200 fall 7.9% in the prior few weeks.

Nobody can say with confidence how high the cash rate will get. However, the RBA seems to have taken a more pragmatic approach by slowing rate hikes and giving time to assess if the recent rate hikes have impacted household spending. It is a delicate balance to reduce 40-year high inflation without pushing the Australian economy into recession.

Ngoc Christodoulou

Associate Financial Planner

Authorised Representative No. 1271825

If you have any questions or comments, please email me at ngoc@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026