WEEKLY E-MAIL

RESERVE BANK OF AUSTRALIA (RBA) HOLDS INTEREST RATES

By Karen Maher

At its meeting on Tuesday, 4 July, the RBA decided to leave the cash rate on hold at 4.10%.

This is just the second meeting since May 2022 in which the RBA decided to keep interest rates on hold.

In his statement released after the board meeting, Governor Philip Lowe said that while inflation was still too high and set to remain so for some time yet, it had “passed its peak”.

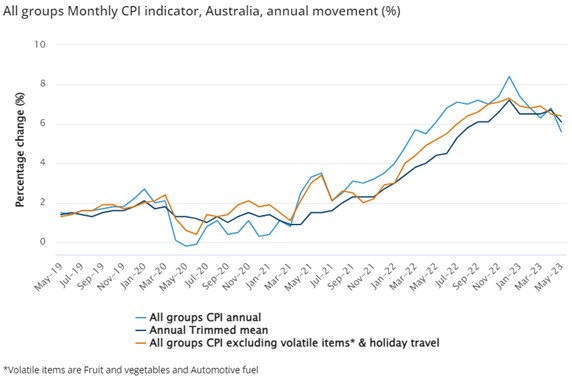

ABS figures showed that the inflation rate in the 12 months to May slowed to 5.6%, which is still well above the RBA’s 2-3% target.

Source: ABS

After 12 near-consecutive rate hikes, and in light of the “uncertainty surrounding the economic outlook”, the bank’s board says the decision will “provide some time to assess the impact of the increase in interest rates to date and the economic outlook”.

The pace of economic activity in Australia has slowed, and although labour market conditions have eased, they still remain tight.

The effects of monetary policy are lagged, and with the largest part of the fixed rate mortgage reset (the ‘fixed rate mortgage cliff’) to higher variable rates only recently occurring in June, many Australians are yet to feel the full force of these rate increases.

The RBA is still expecting the economy to grow as inflation returns to the 2-3% target range, but the path to achieving this balance is a narrow one. Some further tightening of monetary policy, i.e. rate hikes, may be required to ensure that inflation returns to target in a reasonable timeframe, but will depend on how the economy and inflation evolve over the coming months.

At the August meeting, the RBA will have June quarter inflation data which comes out at the end of this month and a revised set of economic forecasts, which may well include faster wages growth given the stronger-than-expected increase in minimum and award wages, as announced by the Fair Work Commission from 1 July 2023.

Many economists are predicting a further two 0.25% rate rises, in August and September, taking the cash rate to 4.6%.

While the interest rate increases place more pressure on mortgage holders, they will benefit self-funded retirees who have their savings invested in cash deposits.

Karen Maher

Associate

If you have any questions or comments, please email me at karen@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026