WEEKLY E-MAIL

LICs vs ETFs: How CGT Changes Could Affect Investors

By Ethan Hardeman

When building a diversified investment portfolio, investors often encounter two popular ASX-listed investment vehicles: Exchange Traded Funds (ETFs) and Listed Investment Companies (LICs).

Whilst both provide access to professionally managed portfolios, they operate under different legal structures and may suit different investor objectives, particularly when tax outcomes are considered.

Listed Investment Company (LIC)

A Listed Investment Company (LIC) is an actively managed investment fund structured as a company and listed on the ASX. Investors purchase shares in the company, which pools capital to invest in a diversified portfolio of assets, including Australian and international shares, fixed-interest securities, and alternative investments.

Unlike trusts, LICs pay company tax (currently 30%) on their taxable income and realised capital gains. After paying tax, profits may be retained within the company or distributed to shareholders as dividends, which may include franking credits.

Advantages of LICs

- Because LICs have a fixed number of shares on issue, their share price is determined by supply and demand. This can create opportunities to purchase a diversified portfolio at a discount to its underlying Net Tangible Asset (NTA) value. Conversely, LICs may also trade at a premium to NTA.

- Many Australian LICs pay regular franked dividends, making them attractive to investors seeking a reliable income stream.

- As investors cannot redeem shares directly with the company, LIC managers are generally not forced to sell investments to meet investor withdrawals during periods of market volatility.

- LICs can retain after-tax profits and franking credits on their balance sheet. These reserves may allow directors to maintain more consistent dividend payments through varying market conditions.

Exchange Traded Fund (ETF)

An Exchange Traded Fund (ETF) is generally structured as a managed investment trust. Some ETFs track a market index while others are actively managed. Investors buy and sell units on the ASX, while authorised participants create and redeem units to keep the trading price close to the underlying Net Asset Value (NAV).

Unlike companies, trusts generally distribute taxable income and realised capital gains directly to investors each year.

Advantages of ETFs

- The creation and redemption mechanism generally keeps an ETF’s trading price close to its underlying NAV.

- ETFs typically provide transparent pass-through of income and realised capital gains to investors.

- Many ETFs offer low management costs, broad diversification and easy access to domestic and international investment markets.

- Many actively managed ETFs combine professional portfolio management with the convenience and liquidity of ASX trading.

- ETFs generally provide regular portfolio and NAV disclosure, offering investors a high degree of transparency.

Proposed Capital Gains Tax Reforms and Their Potential Impact

From 1 July 2027, Australia’s capital gains tax rules will change. Under the legislated reforms, the existing 50% capital gains tax (CGT) discount for individuals and trusts will be replaced with an inflation-indexed methodology together with a minimum 30% tax rate on capital gains accruing from that date. The reforms apply prospectively, meaning capital gains that accrue before 1 July 2027 continue to be taxed under the existing rules.

Under the current tax system, investors receiving capital gains distributed from managed investment trusts, including many ETFs, may benefit from the 50% CGT discount where the underlying assets have been held for more than 12 months.

If the proposed reforms proceed, this concession may be reduced, potentially changing the relative after-tax outcomes between trust and company investment structures.

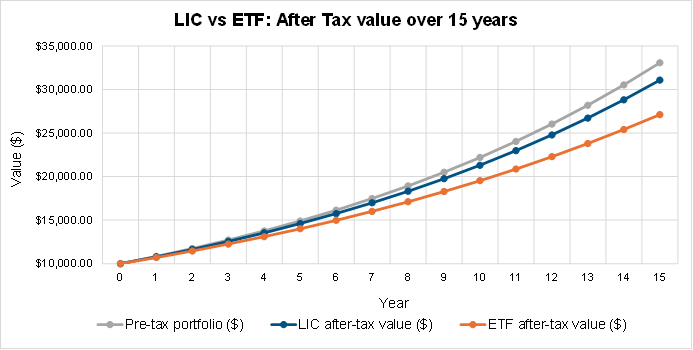

Illustrative Example

Suppose two investors each invest $10,000 in an identical diversified Australian share portfolio and both achieve the same underlying investment return over 15 years.

The first investor holds the portfolio through an ETF. As investments are bought and sold within the fund over time, realised capital gains are generally distributed to investors. Under the proposed reforms, these distributed capital gains may receive less favourable tax treatment than under the current rules, potentially increasing the amount of tax paid by investors over time.

The second investor holds the identical portfolio through an LIC.

The same investment decisions are made, and the same capital gains are realised. However, the LIC pays tax on realised gains at the corporate tax rate before profits become available for distribution. Rather than distributing gains immediately, the LIC may retain after-tax profits and franking credits on its balance sheet and determine when to distribute them to shareholders as franked dividends.

This flexibility may reduce the immediate tax impact on investors and provide greater control over the timing of distributions.

Important: The following example is hypothetical and is provided solely to illustrate how different investment structures may be taxed under the proposed legislation. It is not a forecast of investment performance or an indication that one structure will outperform another. Actual outcomes will depend on investment returns, portfolio turnover, tax rates, franking credits, investor circumstances and the final form of any legislation.

Assumptions

- Initial investment: $10,000

- Identical underlying investment portfolio

- Identical pre-tax investment returns

- Identical portfolio turnover

- Proposed CGT reforms apply throughout

- No additional investments or withdrawals

- Figures are illustrative only

The graph below demonstrates the hypothetical after-tax impact of the proposed tax reforms.

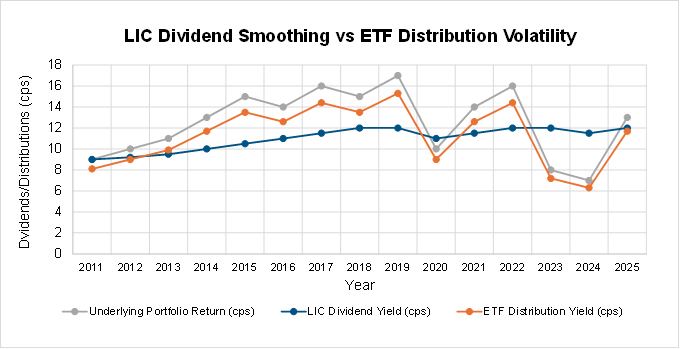

Illustrative Example – Income Stability

The differing legal structures may also influence the pattern of income investors receive.

Because ETFs generally distribute most of their taxable income and realised capital gains each year, distributions often fluctuate with the underlying portfolio’s realised investment gains.

An LIC, by contrast, may retain a greater proportion of earnings during stronger market periods and subsequently use accumulated profit reserves and franking credits to support dividend payments during weaker markets. While dividend levels can never be guaranteed, this flexibility may allow an LIC to maintain a more consistent income stream over time.

The following chart illustrates how this smoothing mechanism may operate.

Conclusion

Both LICs and ETFs continue to play an important role in well-diversified investment portfolios.

ETFs offer pricing that closely tracks net asset value, broad diversification, transparency, liquidity and efficient access to a wide range of investment strategies.

LICs offer a different set of potential advantages, including the ability to retain earnings, accumulate franking credits, smooth dividend payments and, at times, trade at discounts to their underlying asset values.

If the proposed capital gains tax reforms proceed, the relative after-tax outcomes of each structure may change, particularly for long-term investors and those on higher marginal tax rates. However, taxation is only one factor to consider when selecting an investment vehicle.

The most appropriate structure will depend on an investor’s objectives, investment time horizon, income requirements, tax position and overall financial circumstances.

Ethan Hardeman

Junior Paraplanner

If you have any questions or comments, please email me at ethan@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

4 Jun 2026

27 May 2026

21 May 2026