WEEKLY E-MAIL

INTEREST RATES, HOUSE PRICES AND SUPERANNUATION – THE KEYS TO AUSTRALIA’S HOUSEHOLD WEALTH

By James Malliaros

Australia’s household wealth is measured by a household’s assets minus its liabilities.

Household assets comprise financial assets, which include bank deposits, direct shares and superannuation balances, and non-financial assets, which include housing and durable items such as motor vehicles. A household’s liabilities are largely made up of residential mortgages, but also include items such as credit card debt and personal loans.

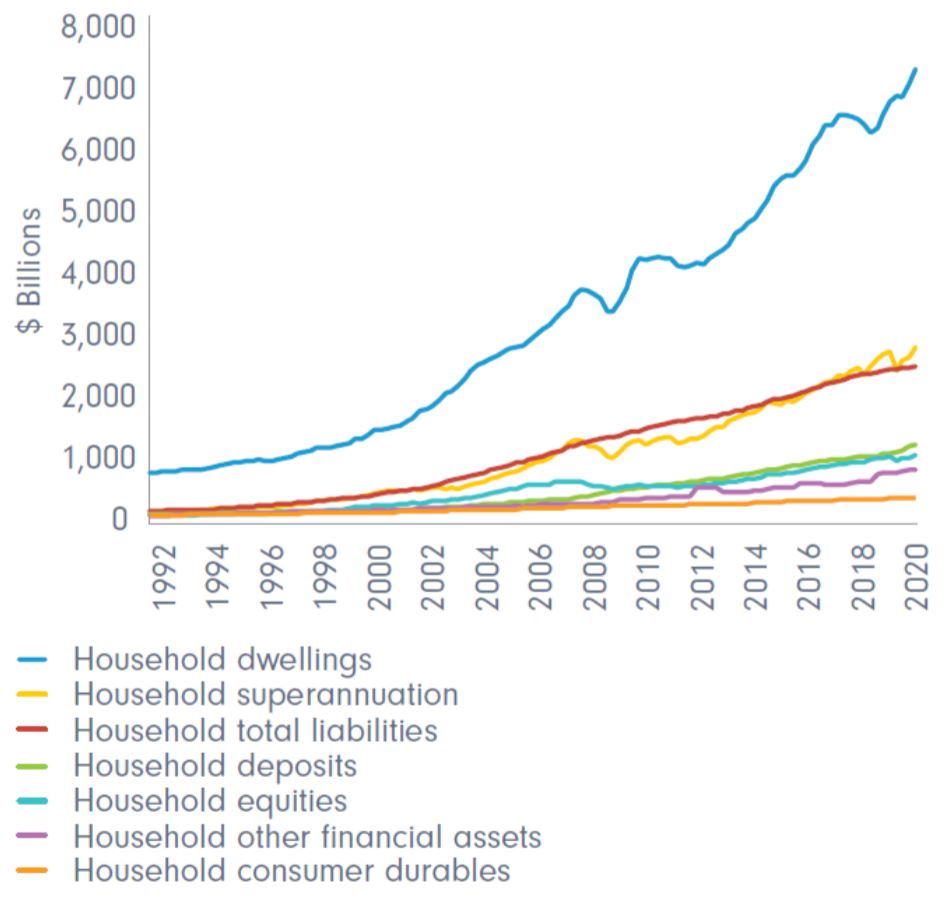

As at the end of 2020, Australian households had amassed around $14 trillion in wealth, while liabilities stood at close to $2.5 trillion, resulting in a net worth position of $11.5 trillion.

The value of the three main components of household wealth were as follows:

- household dwellings – almost $7 trillion

- superannuation assets – $2.8 trillion

- bank deposits – $1.3 trillion.

Interestingly, superannuation has grown from 11% of household wealth in 1989 to 21% today, reflecting an environment of record share prices over the time period, fuelled by ever-lower interest rates.

Australian household wealth (1991 – 2020)

Source: Fidelity International, ABS, RBA, June 2021.

The rate of growth of household wealth has varied greatly from year to year and on several occasions, such as during the Global Financial Crisis and during the COVID pandemic, the value of household wealth actually declined. However, these declines in wealth have been relatively short-lived, as the Reserve Bank of Australia (RBA) has inevitably responded to these economic shocks by cutting interest rates quite significantly.

As is shown in the graph below, whenever the RBA reduces the cash rate, household debt increases, which then pushes up asset values, particularly house prices.

A history of asset price inflation, debt, and the cash rate.

Source: Fidelity International, Bloomberg, RBA, ABS, June 2021.

Ideally, the RBA would prefer higher house prices given the impact it has on consumer confidence and spending. Generally, higher house prices should spur greater consumption, which is normally the largest contributor to economic growth of most of the developed economies in the world. Rising housing prices are often associated with a larger number of housing transactions and typically these households purchase housing-related goods and services in the months before and after a home purchase.

Economists at the RBA have attempted to quantify the impact on consumption from rising wealth. In a paper released in March 2019, RBA analysis suggests that a 1% increase in the value of housing wealth will lead to a 0.16% increase in the long-run level of consumption. Since December 2019, housing wealth has grown by 7.7%, suggesting an uplift in household consumption of 1.1% or around $3 billion. Interestingly, almost half of this spending occurs in the first two quarters after the uplift in housing wealth.

The RBA concluded in its research that when wealth increases, Australian households consume more. Spending on durable goods, like motor vehicles, and discretionary goods, such as recreation, appears to be most responsive to changes in household wealth, although many categories of consumption expenditure appear to grow more quickly when wealth increases. The positive relationship between consumption and wealth is particularly robust for housing wealth and has been stable over time.

The RBA is very aware that lower interest rates lead to higher borrowings, reduced savings, and generate higher house prices. This assists them in meeting their goals in terms of employment and inflation by stimulating consumption. The longer-term question for the Australian economy is whether the rapidly increasing asset prices we’ve seen over the last few years (and subsequent increased levels of household debt) will result in rising financial instability risks in the future, particularly should interest rates need to increase to control potentially rising inflationary pressures.

James Malliaros

Senior Financial Planner

Certified Financial Planner®

SMSF Specialist Advisor™

Authorised Representative No. 291633

If you have any questions or comments, please email me at james@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

27 May 2026

21 May 2026

13 Apr 2026