THE PRACTITIONER

IN THIS ISSUE

- Happy 1st Anniversary!

- Payday Super – Locked In

- The Amended Division 296 Tax

- The 50% CGT Discount: More Than Meets The Eye

- Who Can Make A Claim Against A Deceased Estate?

- Five Changes Impacting Your Super In 2026

- CGT – Buying A New Home Before Selling The Old One

- Permanent Incapacity and Super – What It Means If You’re Totally and Permanently Disabled

- Returning Historical Documents for Safe-Keeping

- Australian Anti Money Laundering & Counter-Terrorism Financing (AML/CTF) Rules

- New Beginnings

Welcome

By Andrew Goldman

It’s a jam-packed edition of The Practitioner, with several excellent articles from the team, which we are sure you will find interesting and informative.

Happy 1st Anniversary!

By Andrew Goldman

Congratulations to Victoria Kong on her recent employment milestone. She is a pleasure to have around the office and an integral part of the team.

Many of you will be familiar with Victoria’s work over the last 12 months, but on such a special occasion, we thought you may like to know a little bit more.

Prior to joining the team at GFM Gruchy, Victoria spent over 20 years working assisting clients with superannuation administration, tax planning, compliance and other complex issues.

Outside of work, Victoria enjoys planning trips overseas, and looks forward to exploring new locations to take in the diversity and beautiful natural landscapes. Victoria is married to Perry and has a daughter Paige who is in enjoying her second year at Uni.

They share their home with a cheeky French Bulldog named Mona.

Payday Super – Locked In

By Ivan Yeung

What is payday super?

Currently, employers are legally required to pay their contributions on a quarterly basis but starting in July 2026, employers must pay superannuation guarantee (SG) contributions to their employee’s super funds at the same time they pay their salary and wages – weekly, fortnightly, or monthly.

Contributions will have to reach employee super funds within 7 days of payday, with the exception of new employees whose first contribution must be paid within 20 days of their first payday.

What this means for employers

All employers, no matter the size, will have to make contributions when they pay their workers. This might affect cash flow, especially for small businesses, and could create an extra administrative burden if they don’t have the right systems in place (such as payroll software, etc).

If you’re an employer, now is the time to start preparing for these changes ahead of their commencement on 1 July 2026. Reviewing your payroll systems and internal processes early will help ensure a smooth transition. This may involve speaking with your payroll software provider, accountant, or registered tax professional to confirm your systems are compliant. If you need support, we’re here to guide you through the process and help you get ready with confidence.

Some employers may need to find alternative payroll software solutions to pay their employees once Payday Super commences as this will coincide with the ATO’s small business clearing house ceasing to be available from 1 July 2026.

ATO’s risk-based approach (first year only)

The ATO will use a practical “traffic light” approach when deciding where to direct compliance effort:

- Low risk: The employer is clearly trying to do the right thing (for example, contributions are made in time but are rejected due to data issues) and the error is fixed promptly so there is no remaining Super Guarantee shortfall.

- Medium risk: The employer doesn’t meet the low-risk criteria, but any shortfalls are fully rectified within a reasonable “catch-up” window after quarter-end.

- High risk: Super Guarantee remains unpaid or underpaid beyond the catch-up window. These cases will be prioritised.

THE AMENDED DIVISION 296 TAX

By Sam Eley

On the last business day of 2025, Treasury released the Bill for the revised, highly-debated Division 296 – Better Targeted Superannuation Concessions measure. The previous Bill aimed to target all members with balances of more than $3m, while the new Bill adds further tax tiers and largely removes the more controversial tax on unrealised capital gains, while adding additional tax measures.

The new Bill puts in place announced changes made by the Federal Treasurer on the 13th October 2025.

There will be two tax tiers for Division 296:

- 15% applied to the portion of earnings that corresponds to the share of the individual’s Total Super Balance (TSB) above $3 million; and

- An additional 10% applied to the portion that corresponds to the share above $10 million

This will mean that the overall tax imposed on superannuation earnings will be as follows:

| Division 296 TSB | Division 296 – Tax Rate on Earnings | Total Effective Tax Rate | |

| Up to $3 million | 0% | 15% | Standard super tax rate |

| $3 million to $10 million | 15% | 30% | 15% + 15% |

| Over $10 million | 25% | 40% | 15% 25% |

The new Bill adds an indexation measure, which was missing from the prior version and was one of the key reasons the previous Bill didn’t progress.

The $3 million threshold will be indexed in increments of $150,000, and the $10 million threshold will be indexed in increments of $500,000.

Another adjustment that has been made is that the revised Bill uses the higher of the individual’s TSB before the start of the income year, and the TSB at the end of the income year. However, this change will also mean that if a member were to die and their TSB at the start of the income year was over $3 million, they will have a Division 296 liability for their relevant portion of Super earnings for the period from the start of the income year to their date of death. In essence, this would be another form of ‘death tax’ for those with higher superannuation balances.

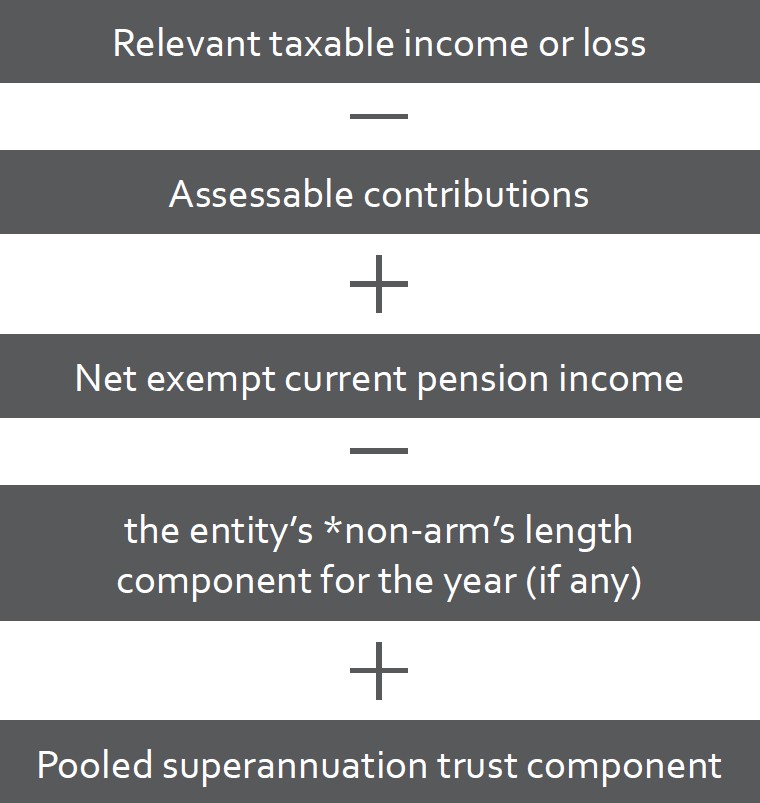

From a tax standpoint, the Government has moved away from the TSB change methodology that was capturing unrealised capital gains to a specific fund level earnings approach. For SMSF’s, super earnings are calculated as follows:

Division 296 is to commence on 1 July 2026, focusing on the TSB as at 30 June 2027. The first Division 296 Notice is expected to be issued in the 2027-2028 financial year.

The 50% CGT discount: More than meets the eye

By Andrew Goldman

There has been much said in the media claiming the 50% capital gains tax (CGT) discount has contributed to the housing affordability problem in Australia, although the problem is a lot more complex than attributing it mainly to any taxation measure or measures.

CGT looms large for anybody who disposes of assets that are subject to CGT, this is clear. However, CGT and the 50% discount may have relevance to your otherwise CGT-exempt home because you may be subject to a partial exemption due to the way you have used it to produce income or in some other cases.

Also, you may inherit a home and not satisfy the requirements for a full CGT exemption.

The rules for applying the discount are not as straightforward as you may think.

For example, in cases where you make a capital gain, you must first apply any prior year or current year capital losses you have before you apply the discount – and this in effect dilutes the value of the discount.

If the capital gain arises from the sale of a business asset and you qualify for the CGT small business concessions, there are other rules to consider before applying the discount if it is available at all.

Importantly, the full 50% CGT discount is generally not available to foreign residents for assets they acquire after 8 May 2012 but an apportionment may be applied for any period of Australian tax residency before becoming a foreign tax resident.

Further, even if you are a resident when you sell an asset, the 50% discount may be lost to the extent you were not a resident during the period you otherwise owned it.

Note that not all taxpayers can use the discount. For example, a company is not eligible for any discount (albeit, it has lower tax rate of either 25 or 30%). And superfunds are only entitled to a 33 1/3% discount.

Likewise, not all capital gains qualify for the discount. Typically, capital gains which arise from granting legal rights to another person or entity do not qualify for the discount – such as gains from granting a restrictive covenant to your employer or granting an easement over land.

Finally, in order to qualify for the CGT discount, you must have owned the asset that gave rise to the capital gain for at least 12 months – and the ATO takes the view that this does not include the day you legally acquired the asset nor the day you sold it.

So, in reality you need to have held the asset for 367 days – or 368 days in a leap year!

As with anything to do with tax, even the CGT discount is not straightforward. So, as always, make sure you seek advice on any such matters.

Who can make a claim against a deceased estate?

By Philip Gruchy

In Australia, the law recognises that a will maker may sometimes fail to make adequate provision for close family or dependants. In that situation, certain people can ask the Supreme Court for a share, or a larger share, of the deceased’s estate. This is usually called a family provision claim or a claim against a deceased estate.

Although each state and territory has its own Act, they all broadly follow the same idea:

- You must be an eligible person, and

- You must show that you’ve been left without adequate provision for your proper maintenance and support.

Who is generally allowed to claim?

The exact list differs slightly by state, but across Australia the following categories are commonly eligible:

1. Spouses and de facto partners

- A husband or wife at the time of death

- A de facto partner who was living with the deceased in a genuine domestic relationship

2. Children

Biological and adopted children are generally eligible in every jurisdiction.

Step-children may be eligible in some states either directly (for example in Victoria and Western Australia) or where they were financially dependent or part of the deceased’s household.

3. Former spouses or partners

Most states allow a former spouse or domestic partner to claim, usually where there has not already been a full and final family law property settlement, or where there are “special factors” warranting an application

4. Other dependants

Many Acts also allow claims by:

- Grandchildren who were financially dependent on the deceased or were, in substance, brought up by them

- Other household members (for example, a step-child, parent, or other relative living in the same household) who were wholly or partly dependent on the deceased

- A person in a “close personal relationship” with the deceased. This might include a long-term carer or companion providing domestic support and personal care. This is most clearly recognised in New South Wales but similar ideas appear elsewhere

Being eligible is only the first step

Even if you fit into one of these categories, the Court will not automatically change the will. It must decide whether, after looking at all the circumstances, adequate provision has been made for you.

Across Australia, courts generally look at similar factors, such as:

- The nature and length of your relationship with the deceased

- Any obligations or responsibilities the deceased had towards you (compared with other beneficiaries)

- The size and nature of the estate

- Your financial position, health, age and future needs

- Any significant contributions you made to the deceased or their property

- Any gifts or support you already received during the deceased’s lifetime

- Any serious misconduct or long-term estrangement, in appropriate cases

Judges often talk about “what a wise and just” person, or what the “community” would generally regard as fair in the circumstances would have done, without simply rewriting the will from scratch.

Time limits and next steps

Time limits to make a family provision claim are strict and vary by state. The Court will only extend time beyond these time limits in limited situations.

If you think you may have a claim, it is generally sensible to get prompt advice from a wills and estates lawyer.

Five changes impacting your super in 2026

By Kerry Taylor

Superannuation rules are always evolving, and 2026 is shaping up to be another year of important changes. Some of these updates may only affect a small group of people, while others could impact almost everyone with super.

Whether retirement feels a lifetime away or it’s already on the horizon, understanding what’s changing can help you make smarter decisions and avoid costly mistakes. Here are six key changes to keep on your radar.

1. Tax changes for large super balances

One of the most talked-about changes is the increased tax on large super balances, also known as Division 296 tax, which is detailed earlier in this newsletter.

Under the legislation, the tax rates will be as follows:

- Balances up to $3 million: no change. Earnings continue to be taxed at 15% as they are now.

- Balances between $3 million and $10 million: an extra 15% tax on earnings, bringing the total to 30% on that portion.

- Balances above $10 million: the total tax rate on earnings will rise as high as 40%.

It’s important to note:

- These changes are not law yet

- Only a small number of Australians would be affected

- Withdrawing super prematurely can be hard to undo because of contribution limits

If this may apply to you, get professional advice before making any big moves.

2. Contribution caps are expected to increase

Thanks to rising wages, super contribution limits are expected to increase from 1 July 2026.

While final confirmation depends on official figures released in late February 2026, the changes are widely expected to be:

- Concessional (before-tax) cap increasing to $32,500

- Non-concessional (after-tax) cap increasing to $130,000

These caps are linked to wage growth, and based on recent data, it would take a significant and unlikely drop in wages for indexation not to occur.

This change could create opportunities for:

- People topping up their super

- Those who arrange with their employer to salary sacrifice part of their income into super

- Individuals planning larger after-tax contributions

Once the new caps are confirmed, we’ll let you know and help you understand what they mean for your super strategy.

3. Transfer balance cap: what’s happening next?

The transfer balance cap (TBC) limits how much super you can move into a retirement-phase pension. Unlike contribution caps, the TBC is indexed to inflation (CPI) rather than wages.

Based on the latest December CPI figures, the TBC is set to increase from $2 million to $2.1 million from 1 July 2026.

This change will mainly affect people who haven’t yet started a retirement pension. If you already receive a retirement pension from your super, you may still benefit from a partial increase, depending on your individual circumstances and how much of your cap you’ve already used.

4. More flexibility for legacy pensions

There is some good news for people holding older super pension products.

New rules now allow greater flexibility for certain legacy pensions, such as lifetime, life expectancy and market-linked pensions held in SMSFs.

Previously, these pensions:

- Couldn’t be easily changed or exited

- Often no longer suited members’ needs

- Had strict limits around reserves and conversions

Under the new rules:

- A five-year window allows eligible members to review and restructure these pensions

- This creates opportunities to simplify super and improve flexibility

Because legacy pensions are complex, professional advice, especially from an SMSF specialist, is strongly recommended before making changes.

5. Better fund performance, transparency and tech

Large APRA-regulated super funds continue to face increased scrutiny, and that’s a win for members.

In 2026, expect to see:

- Ongoing pressure on underperforming funds, including forced mergers

- Clearer reporting on fees, performance and investments

- Better tools to compare super funds and make informed choices

At the same time, technology is transforming how we interact with super. Many funds are rolling out:

- Smarter online dashboards

- Improved mobile apps

- AI-driven tools to help with investment choices and retirement planning

If you haven’t logged into your super account lately, 2026 is a good year to start.

Final thoughts

Superannuation is a long-term game, and even small rule changes can have a big impact over time.

Take the time to review your super, stay informed about potential changes, and consider speaking to a financial adviser if needed. With the right knowledge and strategy, you can make sure your super keeps working hard for your retirement.

CGT – Buying a new home before selling the old one

By Andrew Goldman

If you find yourself in the position of having bought yourself a new home before selling your existing home, there are important CGT issues to consider – and these centre on the fact that under the CGT rules, you cannot have two or more CGT exempt homes at the same time.

However, there is an important concession that allows you to treat both the new home and the existing home as exempt from CGT for up to a period of six months – provided the new home actually becomes your main residence.

So using a simple example, where you bought your new home on 1 February 2026 and then sell your existing one five months later on 1 July 2026, your existing home won’t be subject to any CGT – and your new home won’t lose any CGT exemption for this five month period.

However, the availability of this concession is subject to a number of important conditions.

Firstly, the existing home must have been your home for a period of at least three months in the 12 months period before you sold it. And, secondly, it must not have been used for the purpose of producing taxable income in any part of that 12 month period when you did not live in it.

So, in the above example, if you rented your existing home in the five month period before you sold it (which vendors sometimes do while waiting to sell it), you could not use this concession to give you an additional five months of exemption on that home. As a result, you will be subject to a partial CGT liability to reflect the fact that your dwelling could not be treated as a main residence during this five month period.

It is worth noting that if this was the first time you rented the existing home and it would otherwise have been entitled to a full main residence exemption just before you rented it, then you would calculate this partial CGT liability by reference to its market value when you first rented it and the amount you sell it for.

There are other concession available, such as the “absence concession” and the “building concession”, however, in both these cases the application of these particular concessions, and their interaction with the rule that allows you to treat an existing home and new home as CGT exempt for up to six months, can be quite complex. And much will depend on the precise facts of the case.

If you find yourself in the position of having bought yourself a new home before you sold your old one (or are intending to do this) speak to us – and we will show you how the rules operate in your circumstances, and how they can be applied most advantageously.

Permanent incapacity and super – what it means if you’re totally and permanently disabled

By Victoria Kong

Most people think of superannuation as money they can’t touch until retirement, but there are important exceptions. One significant exception is the permanent incapacity condition of release, which can allow people who are totally and permanently disabled to access their super earlier.

Understanding how this works can make a real difference at a time when income, medical costs, and financial security are often under pressure.

What is permanent incapacity?

Under superannuation law, permanent incapacity generally means that, because of physical or mental ill-health, you are unlikely to ever work again in a job for which you are reasonably qualified by education, training, or experience.

To meet this condition of release, your super fund usually requires certification from two medical practitioners confirming that your condition is permanent and prevents you from returning to suitable employment.

Once this condition is satisfied, your super can be released to you, even if you are well below preservation age.

You can access super even without insurance

A common misconception is that you can only receive money from super if your fund held Total and Permanent Disability (TPD) insurance. That’s not the case.

Even if your super fund did not have any insurance cover at all, you may still be able to access:

- Your existing super balance

- Employer contributions

- Personal contributions and earnings

The permanent incapacity condition of release applies to your super savings themselves, not just to insurance payouts. This can be especially important for individuals who changed jobs frequently, had low balances, or opted out of insurance.

In other words, the absence of insurance does not prevent access to super if you meet the permanent incapacity rules.

How the money can be paid

Once approved, the released super can usually be taken as:

- A lump sum, which may assist with large expenses like paying off the mortgage

- An income stream which may assist with meeting ongoing living expenses

Tax treatment may vary depending on your age and the components of your super, but in most cases, part of the benefit will be taxed concessionally compared to regular income.

It is important to get advice about your options and any tax implications before payment.

The role of TPD insurance in super

While insurance is not required to access super under permanent incapacity, TPD insurance held inside super can provide significant additional support.

If your fund includes TPD cover and your claim is accepted, the insurance benefit is paid into your super account. This can substantially increase the amount available to you, often at a time when earning an income is no longer possible.

Some key benefits of TPD insurance in super include:

- Premiums are generally deductible to the fund and this benefit is passed on to the member

- Premiums are paid from super, not your take-home pay meaning it won’t impact your cashflow

- You may not have to deplete super savings otherwise set aside for retirement

Final thoughts

The permanent incapacity condition of release from super exists to provide financial support when it’s needed most. If you are totally and permanently disabled, superannuation is not locked away indefinitely and can be accessed to help you manage life after work.

Whether or not insurance is involved, understanding your options can ease financial stress and give you more control during a difficult time. If you think you may qualify, speak to us to help guide you through your next step with confidence.

Returning Historical Documents for Safe-Keeping

By Bonnie Collins

Over the last 6-12 months, we have been undertaking a project to reduce our waste and carbon footprint and to limit our retention of historical documents.

As this project draws to a close, we feel proud that we have made significant progress towards being a paper-free office by changing our internal workflow processes and scanning and archiving many thousands of pages of documents.

As with any plan, there are some exceptions to the scan and archive process and these relate to original documents which must be retained in hard copy form. Things such as Trust Deeds, company constitutions and other establishment and certain capital gains tax related documents to name a few examples.

If we are holding documents on your behalf, we will likely be in touch with you over the next 4 – 6 weeks to make arrangements for the collection or return of your documents.

Australian Anti Money Laundering & Counter-Terrorism Financing (AML/CTF) Rules

By Andrew Goldman

From 1 July 2026, new AML/CTF reforms—known as “Tranche 2”—will bring many accounting services under Australia’s AML/CTF regime. This means accountants will have new legal obligations aimed at preventing money laundering and terrorism financing.

Why these rules affect you as a client

Australia is expanding AML rules to include accountants because many accounting activities—such as setting up companies, managing funds, or providing business addresses—can be used (even unknowingly) to hide or move illicit money. These reforms align Australia with global standards.

As a result, when you engage an accountant for certain services, they may be legally required to verify your identity, understand the purpose of transactions, and request additional documents—not because they distrust you, but because the law requires it.

Accountants must follow specific processes to comply with the law:

1. Customer Due Diligence (CDD)

Accountants must confirm:

- Who you are (identity verification)

- What you are doing (purpose of the service or transaction)

- Where funds are coming from (source of funds or wealth in higher risk cases)

This is required both before engaging in the service and on an ongoing basis. To ensure we fully comply with our obligations, we will likely undertake a project to update and confirm previously verified identity documents and details.

Depending on your risk profile, we may apply:

- Simplified checks for low risk clients

- Enhanced checks for higher risk clients (such as politically exposed persons or complex structures)

2. Requests for additional information or documentation

We may ask for:

- Identification documents (such as a passport or driver licence)

- Proof of address

- Trust deeds or company constitutions

- Details on business activities

- Source of funds or source of wealth information

- Explanations for unusual transactions

These requests are not optional—they are a legal requirement to help us comply with AML laws.

3. Reporting obligations

Accountants must report to AUSTRAC if we identify:

- Suspicious activities

- Large transactions, depending on thresholds

- Other reportable matters under the Act

Why these rules protect you

Although the checks may feel intrusive, they help

- Protect you and us from association with financial crime

- Safeguard Australia’s financial system

- Ensure compliance with global standards

What you can do to make the process smooth

- Provide requested documents promptly

- Be transparent about ownership structures and the purpose of transactions

- Keep company or trust documentation up to date

- Expect occasional follow-up questions, especially if your circumstances change

New Beginnings

By Andrew Goldman

After 10 years at 190 Through Road, Camberwell, the continued growth of GFM Wealth and GFM Gruchy Accounting has prompted a move to a larger, modern office space at Level 2, 141 Camberwell Road, Hawthorn East.

A key priority in selecting our new premises was ensuring it is both client- and staff-friendly, providing comfort, accessibility, and convenience for all. Located only 4 km from our current office and close to Camberwell Junction — almost opposite the Rivoli Theatre — the new location offers several advantages, including:

- Secure on-site parking beneath the building with direct lift access to Level 2

- A café located on the ground floor

- Easy access to public transport, shops, cafés, and restaurants at Camberwell Junction

The office is currently in the final stages of a full refurbishment, with our move scheduled for early to mid-May. To minimise disruption during this period, all client meetings throughout May will be conducted online via Zoom or Microsoft Teams. Our team may also work remotely at times while IT and building access systems are finalised.

We look forward to welcoming clients to the new office from June onwards. As the move approaches, we will keep you informed of key details and will provide clear instructions regarding parking and building access ahead of your first visit to ensure a smooth transition.

This relocation represents an important milestone for our business, and we are excited to share our new space with you.

We look forward to seeing you soon at our new office.

This publication is for guidance only, and professional advice should be obtained before acting on any information contained herein. Neither the publishers nor the distributors can accept any responsibility for loss occasioned to any person as a result of action taken or refrained from in consequence of the contents of this publication. Publication March 2026.

Edition #22

Edition #21

Edition #20