WEEKLY E-MAIL

THE INTEREST RATE RISES ARE NOT OVER…

By Patrick Malcolm

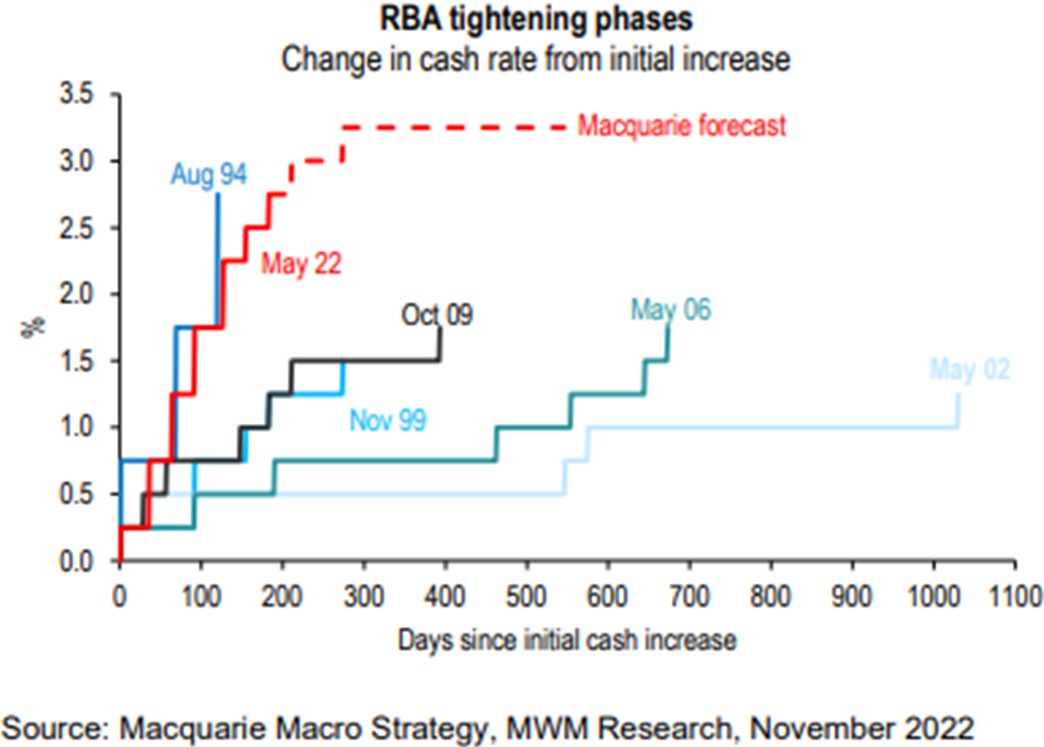

Since May 2022, the Reserve Bank of Australia has raised the cash rate by 275 basis points, up to 2.85%, the highest level in nearly a decade and at the fastest pace since 1994.

It is not an exaggeration to say that many Australians have never seen such heavy rate rises in succession and the effect this will have on household income.

The bad news is that the pain for households is not over and will likely persist well into next year.

In his most recent press conference, Governor Philip Lowe signalled that more tightening is expected as inflation in Australia remains too high. While the Australian economy has remained robust despite rising interest rates, Australia’s inflation backdrop looks similar to global developed market peers.

Inflation is expected to peak at 8% late in 2022, up on the 7.8% projected back in August. Conversely, growth over 2023 and 2024 is now projected at 1.5%, down from the initial estimates of 1.8% a few months ago. The market is now pricing in a cash rate of 4.0% in July 2023, indicating we still have 1.15% raises in the ensuing months.

The revisions to forecasts show the difficulty facing all central banks. Once in the system, inflation is difficult to forecast with certainty. Unless a substantial price decline towards target levels occurs, central banks will have to continue tightening monetary policy.

Why is curbing inflation so important? Because beyond the challenges of a higher cost of living, inflation also poses risks to financial stability and risk management within markets. The key domestic factors that the RBA will be focusing on are:

- Wages: While Australia’s wage growth remains below other advanced economies at 2.60% p.a, the RBA is focused on avoiding a price-wage spiral that becomes entrenched.

- Labour Market: Unemployment levels remain at 50-year lows at just 3.50% p.a. A tight labour market keeps demand for labour elevated (as there is a lack of supply) and adds to wage pressures. A fully employed economy also adds to inflationary pressures, as they will keep spending.

- The breadth of inflation: The RBA will continue to focus on if inflation is expanding into areas that may result in price “stickiness”, such as rents, which are harder to unwind.

From a global perspective, the RBA will also be keeping watch on what the US Federal Reserve continues to do. The US drives global monetary conditions – a rising US dollar and expectation of a 5% US cash rate are working to tighten global financial conditions and slow demand, which will flow onto Australia.

Geopolitical tensions around the conflict in Ukraine will continue to be a concern on many fronts, but from an inflationary perspective, energy and food prices are likely to remain elevated.

China’s slowing economic growth due to continued COVID-19 restrictions and negative sentiment around their property sector will also impact Australia, given China is our largest trading partner.

This is a complex issue, and the story still has a long way to go. We expect volatility to continue until there is clarity that inflation has peaked, with no upward surprises, and that the aggressive interest rate hikes are working as intended.

Patrick Malcolm

Senior Partner

Certified Financial Planner®

SMSF Specialist Advisor™

Barron’s Top Financial Adviser 2020

Authorised Representative No. 278061

If you have any questions or comments, please email me at patrick@gfmwealth.com.au

Disclaimer: This document is not an offer or invitation to any person to buy or sell any interest in or deposit funds with any institution. The information here is of a generic nature, and does not take into account your investment objectives or financial needs. No person should act upon this information without firstly seeking competent, professional advice specifically relating to their own particular situation.

Copyright: © This publication is copyright. Subject to the conditions prescribed under the Copyright Act, no part of it may, in any form, or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission. Enquiries should be addressed to GFM Wealth Advisory.

27 May 2026

21 May 2026

13 Apr 2026